Leverage (finance)

From Wikipedia, the free encyclopedia

|

|

This article needs additional citations for verification. Please help improve this article by adding reliable references (ideally, using inline citations). Unsourced material may be challenged and removed. (July 2008) |

In finance, leverage (or gearing due to its analogy with a gearbox) is borrowing money to supplement existing funds for investment in such a way that the potential positive or negative outcome is magnified and/or enhanced.[1] It generally refers to using borrowed funds, or debt, so as to attempt to increase the returns to equity. Deleveraging is the action of reducing borrowings.[1]

In macroeconomics, a key measure of leverage is the debt to GDP ratio.

Contents |

[edit] Types of leverage

[edit] Financial leverage

Financial leverage (FL) takes the form of a loan or other borrowings (debt), the proceeds of which are (re)invested with the intent to earn a greater rate of return than the cost of interest. If the firm's rate of return on assets (ROA) is higher than the rate of interest on the loan, then its return on equity (ROE) will be higher than if it did not borrow because assets = equity + debt (see accounting equation). On the other hand, if the firm's ROA is lower than the interest rate, then its ROE will be lower than if it did not borrow. Leverage allows greater potential returns to the investor than otherwise would have been available but the potential for loss is also greater because if the investment becomes worthless, the loan principal and all accrued interest on the loan still need to be repaid.

Margin buying is a common way of utilizing the concept of leverage in investing. An unleveraged firm can be seen as an all-equity firm, whereas a leveraged firm is made up of ownership equity and debt. A firm's debt to equity ratio is therefore an indication of its leverage. This debt to equity ratio's influence on the value of a firm is described in the Modigliani-Miller theorem. As is true of operating leverage, the degree of financial leverage measures the effect of a change in one variable on another variable. Degree of financial leverage (DFL) may be defined as the percentage change in earnings (earnings per share) that occurs as a result of a percentage change in earnings before interest and taxes.

[edit] Measures of financial leverage

[edit] Debt-to-equity

Debt to equity is generally measured as the firm's total liabilities divided by shareholders' equity. In the following, D = liabilities, E = equity, A = total assets, EBIT = Earnings before interest and taxes and Interest = Interest payment:

- Debt-to-equity ratio =

- Debt-to-value ratio =

= Debt-to-assets[2]

= Debt-to-assets[2]

- Interest coverage ratio =

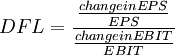

[edit] Degree Of Financial Leverage (DFL)

Financial Leverage affects the EPS of the firm. Financial Leverage acts as a double-edged sword. If the economic conditions are favorable and EBIT is increasing, a higher financial leverage has a positive impact on the EPS. The DFL captures this relationship between EBIT and EPS. DFL is defined as the percentage change in EPS for a given percentage change in EBIT.

Symbolically,

For different applications of leverage, analysts may include or exclude certain items, such as non-tangible balance sheet items, non-financial liabilities, and similar items, or may adjust the carrying value of other items. It is not uncommon to use only financial liabilities (long-term and short-term borrowings), thereby excluding, for example, accounts payable.

[edit] Gearing and Du Pont Analysis

Use of the Du Pont Identity requires that leverage be measured in terms of total assets divided by shareholders' equity, and this is sometimes referred to as gearing or simply leverage:

- Leverage (gearing) = A / E

The two measures are related. Since the terms used are the same throughout, debt-to-equity is equal to gearing times debt over assets: D / E = (A / E) * (D / A)

[edit] Operating leverage

Operating leverage reflects the extent to which fixed assets and associated fixed costs are utilized in the business. Degree of operating leverage (DOL) may be defined as the percentage of leveraging.

[edit] Combined stand-alone leverage

If both operating and financial leverage allow us to magnify our returns, then we will get maximum leverage through their combined use in the form of combined leverage. Operating leverage affects primarily the asset and operating expense structure of the firm, while financial leverage affects the debt-equity mix. From an income statement viewpoint, operating leverage determines return from operations, while financial leverage determines how the “fruits of labor” will be divided between debt holders (in the form of payments of interest and principal on the debt) and stockholders (in the form of dividends). Degree of combined leverage (DTL) uses the entire income statement and shows the impact of a change in sales or volume on bottom-line earnings per share. Degree of operating leverage and degree of financial leverage are, in effect, being combined.

[edit] Correlation leverage

Correlation leverage is a third concept that captures the degree to which the variability in the firm's value is correlated with the variability of the universe of all risky assets.

[edit] Derivatives

Derivatives allow leverage without borrowing explicitly, though the "effect" of borrowing is implicit in the cost of the derivative.

- Buying a futures contract magnifies your exposure with little money down.

- Options do the same. The purchase of a call option on a security gives the buyer the right to purchase the underlying security at a given price in the future. If the price of the underlying security rises, the value of the call option will rise at a rate much greater than the value of the underlying security. However if the rate of the call option falls or does not rise, the call option may be worthless, involving a much greater loss than if the same money had been invested in the underlying instrument. Generally speaking, a put option allows the holder (owner), the investor, to achieve inverted-leverage and/or inverted enhancement--- sometimes called inverse enhancement and/or inverse leverage.

- Structured products that exist as either closed-ended funds, or public companies, or income trusts are responding to the public's demand for yield by leveraging.

[edit] Risk and overleverage

Employing leverage amplifies the potential gain from an investment or project, but also increases the potential loss. Interest and principal payments (usually certain ex-ante) may be higher than the investment returns (which are uncertain ex-ante).

This increased risk may still lead to the optimal outcome for the entity or person making the investment. In fact, precisely managing risk utilizing strategies including leverage and security purchases, is the subject of a discipline known as financial engineering.

There are economic periods when optimism incites to a widespread and excessive use of leverage, what is called overleverage. One of its forms, associated to the subprime crisis, was the practice of financing homes with no or little down payment, playing on the hope that the price of the assets (the property in this case) will rise. Another form involved the five largest U.S. investment banks, which borrowed funds to invest in mortgage-backed securities, increasing their leverage between 2003-2007 (see diagram). During September 2008, the five largest firms either went bankrupt (Lehman Brothers), were bought out by other banks (Merrill Lynch and Bear Stearns) or changed to commercial bank holding companies, subjecting themselves to leverage restrictions (Morgan Stanley and Goldman Sachs).

[edit] Negative gearing

Negative gearing is a form of financial leverage where an investor borrows money to buy an asset, but the income generated by that asset does not cover the interest on the loan. A negative gearing strategy can only make a profit if the asset rises in value and creates enough future capital gains to cover the shortfall between the income and interest that the investor suffers. The investor must also be able to fund that shortfall until the asset is sold. The tax treatment of interest expenses and future gain will also affect the investor's final return.

[edit] Math Example

[3]Calculate equity return given:

5% Projected Return on Investment 4% Cost of Debt 8:1 Leverage Debt:Equity

LONG-FORM MATH

Investment (8+1) * 5% = 45 less Interest (8) * 4% = 32 equals Equity 1 * 13%= 13

SHORT-FORM GENERIC CALCULATION

Interest Rate Differential (5-4) = 1% Debt to Equity Multiple (8/1) = 8 Multiply Line1 * Line2 (1*8) = 8% Add Investment Return + 5% Equals Total Return (8+5) = 13%

[edit] See also

[edit] References

- ^ a b BBC . The layman's finance crisis glossary. Retrieved 2008-10-23

- ^ As A = D + E, by the accounting equation.

- ^ Math for calculating leverage effects

[edit] External links

|

|||||||||||||||||||||||||||||||