Covered call

From Wikipedia, the free encyclopedia

|

|

This article is in need of attention from an expert on the subject. WikiProject Business or the Business Portal may be able to help recruit one. (November 2008) |

A covered call is a transaction in which the seller of call options already owns the corresponding amount of the underlying instrument, such as shares of a stock or other securities. These owned shares provide the "cover" as they can be handed over to the buyer of the options when he decides to exercise them, instead of having to buy the optioned shares at unfavorable market prices in the case of "uncovered" or short call. Thus, the covered call limits the (potentially unlimited) loss that results from a short call when the price of the underlying stock moves above the strike price of the option.

Writing a covered call will generate income, in the form of the premium paid by the option buyer, when the stock price remains stable. However, the risk of stock ownership is not eliminated if the price were to decline. In such a case, potential loss (which can be as high as the purchase price of the security) is reduced by the amount of the premium. Also, the covered call limits the potential profit if the stock price raises above the strike price - the option seller is obligated to sell the underlying stock at the strike price to the option buyer and cannot realize the additional gains.

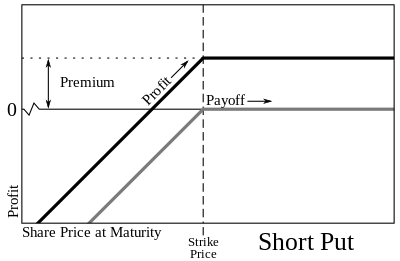

Payoffs on the stock are always the same, as with a short put option, hence the price (or premium) should always remain the same, as with a short put or naked put.

[edit] Examples

An investor has 500 shares of XYZ stock, valued at $10,000. He sells 5 call option contracts for $1500, thus covering a certain amount of decrease in the XYZ stock (i.e. only after the stock value has declined by more than $1500 would the investor lose money overall). Losses can not be prevented, but merely reduced in a covered call position. If the stock price drops, it will not make sense for the option buyer to exercise the option at the higher strike price since the stock can now be purchased cheaper at the market price, and the seller (writer) will keep the money paid on the premium of the option, thus reducing his loss from a maximum of $10000 to $10000 - (premium).

This "protection" has its own disadvantage in which the investor is forced to sell his stock if the option is "called out" in which the writer is forced to sell his stock below market price or he must buy the calls back at a higher price than he sold them for.

The investor might repeat the same process again next month if he/she believes that stock will either fall or be neutral, if before expiration stock price does not reach strike price.

A call can be initiated sometimes even without ownership of underlying stock. If XYZ trades at $33 and $35 call trades at $1, than either can purchase 100 shares of XYZ and only sell one call. For this only $3200 is required to purchase the stock rather than $3300. The premium received for the call covers the decline made by the first $100 ($1 per share) in stock price. Thus $32 stock price is break-even point of the transaction. If the results are high, then profit and lower result means loss. In the above case, the upside potential limits more than $300 ($100 for selling call and $200 for increase in share price) to 35, which amounts to almost 10% return. The investor might repurchase the stock because he cannot participate, as he is required to sell call to 35. So he sell calls at higher strike price.

To summarize:

| Stock price at expiration |

Net profit/loss | Comparison to simple stock purchase |

|---|---|---|

| $30 | (200) | (300) |

| $32 | 0 | (100) |

| $33 | 100 | 0 |

| $35 | 300 | 200 |

| $37 | 300 | 400 |

[edit] Marketing

This marketing strategy is sometimes categorized as "safe" or "conservative" and even "hedging risk" as it provides high income and its flaws are well known since 1975 when Fischer Black published his theory in "Fact and Fantasy in the Use of Options. According to Reilly and Brown (2003); "to be profitable, the covered call strategy requires that the investor guess correctly that share values will remain in a reasonably narrow band around their present levels." (p. 995)

In recent years, the interest in covered call strategies has been enhanced by two developments according to the article “Buy Writing Makes Comeback as Way to Hedge Risk.” Pensions & Investments, (May 16, 2005): (1) in 2002 the Chicago Board Options Exchange introduced the first major benchmark index for covered call strategies, the CBOE S&P 500 BuyWrite Index (ticker BXM), and (2) in 2004 the Ibbotson Associatesconsulting firm published a case study on buy-write strategies. After mid-2004, there was introduction of many new covered call investment products.

Even though there is limited upside and the premium is subtracted, covered calls do not suffer loss as there is complete risk of loss. Selling a naked put is similar to covered calls. Option beginners and many brokerages always categorize naked put as risky. However, a common short put strategy allowed by many firms as a suitable transaction to beginning option traders is a cash covered put.

[edit] References

- Discover Covered Calls [1]

- Chicago Board of Options Exchange [2]

- Screen market for covered calls [3]

|

||||||||||||||||||||||||||||||||||